The SEPA Direct Debit upgrade creditors have been waiting for...

Finally... Over the last three years, we’ve heard hundreds of creditors using SEPA Direct Debits complain about two things. The first thing they complain about is the “First and Recurrent” problem. I don’t want to bet on the number of nightmares collection managers had after trying to figure out how this issue could ideally be solved.

The second thing they complain about is the risk and timing issue related to “CORE” Direct Debits.

These two issues will be tackled on November 20th, the date when the SEPA Direct Debit system will finally meet the market needs. Let me dig further into both problems and tell you what will change on that day.

First & Recurrent Problem

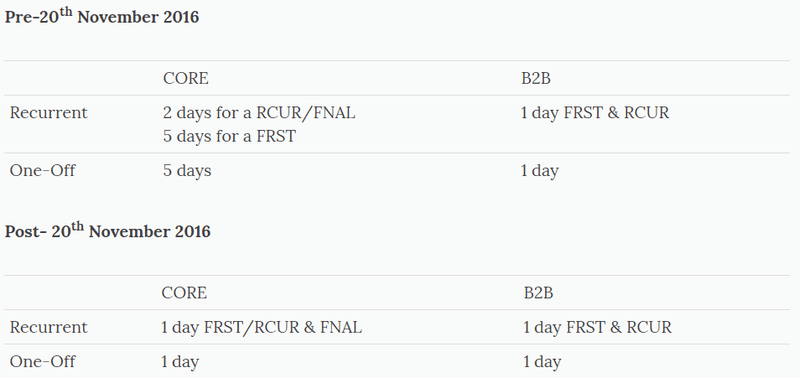

Up until November 2016, it is mandatory to observe a sequence type when collecting a SEPA Direct Debit. The first time a creditor wants to collect a SEPA Direct Debit, he has to deliver a “FRST” instruction to the bank. He then has to wait for this “FRST” instruction to be successfully executed to be sure that his subsequent “RCUR” transactions will be accepted.

Although this is not an issue on a technical level, this way of working does not meet the actual business needs. Companies often have 2 or more SEPA Direct Debits for the same customer which they want to execute immediately. When two transactions, a “FRST” and a “RCUR”, are delivered at the same time to the bank for the same client, there is always a risk that the bank takes the “RCUR” and refuses it. Try figuring out what happens then…. The number of days lost by collection managers, IT support and people responsible for the invoices or CFO’s has a major impact on the internal costs of companies.

This is especially an issue with B2B’s as paper B2B mandates need to be registered at the bank. Multiple retries of a FRST are not unusual in this case.

On top of that, the first collection for a Core SEPA Direct Debit had to be transferred at least five days in advance, which forces collection managers to work with long periods of uncertainty. A lot of ERP and accounting packages don’t even make a distinction between a first CORE and a first B2B Direct Debit and transfer both with the five day delay although this is not needed for a B2B.

Changes to the First & Recurrent sequence types

The difference between First & Recurrent will disappear for both CORE and B2B SEPA Direct Debits! You can continue to use them but it will not have an effect on the processing of the bank. The field in the SDD XML (attribute ‘The Transaction/Sequence Type’) must still be filled in but we suggest you to always use the type RCUR.

The Final (FNAL) sequence type, if used, will also be RCUR.

Changing timing to the CORE scheme

Creditors know very well that the timing for the execution of SEPA Direct Debits is D (due date)-5 for First and D-2 for Recurrent Collections. On November 20th, this will become D-1 for both types and this will be applied to both Recurrent and One-Off SEPA Direct Debits.

See the graph below for an overview of the changes:

The new timing scheme is a lot easier to remember. However, there is one crucial point to bear in mind.**Keep an eye on the cut-off times of your bank!**For some banks, a batch of more than 75000 transactions must be delivered and signed before 6am. So ask your bank for its cut-off time schedule. Our advice to avoid these problems is to continue delivering on D-2 bank business days which will ensure you’re always on time.

Is it mandatory to change something to the internal back office?

There is no need to change anything to the internal back office or collection engine. The feedback will be delivered faster and if you accidently deliver a first & recurrent collection instruction together, this will no longer cause problems as was the case in the past! On the collection date level also, the dates you used to work with will continue to work. The AG02 R-message “incorrect sequence type” will no longer be given as feedback. There is no need to change anything to the internal back office or collection engine. The feedback will be delivered faster and if you accidently deliver a first & recurrent collection instruction together, this will no longer cause problems as was the case in the past! On the collection date level also, the dates you used to work with will continue to work. The AG02 R-message “incorrect sequence type” will no longer be given as feedback.

There is only one change for parties using COR1. Over the last years, COR1 has been introduced in some countries as an alternative scheme to execute SEPA Direct Debits faster. With the introduction of the shorter timings on November 20th, COR1 will cease to exist and will be replaced again by CORE. This is only mandatory for parties using COR1. Over the last few years, COR1 has been introduced in some countries as an alternative scheme to execute SEPA Direct Debits faster (e.g. Germany). With the introduction of shorter timings on November 20th, COR1 will cease to exist and will be replaced again by CORE.

Other changes you should be aware of

It might be seen as a small change, but on November 20th the BIC code will no longer be mandatory on the mandate and in the communication to the bank (except for Monaco and Switzerland).

The consequence of not needing a BIC code also means that when a debtor changes of account or of bank and the underlying account, it will be very difficult for a creditor to know whether this is a real switch of bank or only a switch of the account within the same bank. This is the reason why this change has been done on format level. The meaning of the SMNDA attribute has changed from “Same Mandate New Debtor Agent ” to “Same Mandate New Debtor Account”. The location where this info is normally given by the creditor moves from 2.58 OriginalDebtorAgent to 2.57 OriginalDebtorAccount which can be used for communicating the change for Core and B2B mandates.

Neither the EPC nor the national instances have issued any guideline regarding the signature on a B2B mandate or an electronically signed Core or B2B mandate. In both cases when changing from one bank to another it will be important to sign a new mandate as the registration needs to be done correctly upfront at the debtor bank side. Knowing the relationship between the bank and the bank account remains important for this purpose. For Core mandates negotiated on paper without electronic signature, the SMNDA change will work.

Sunday November 20th: SEPA Direct Debit day

We at Twikey have already seen some banks finishing their development during Q2 of 2016 and for some banks the new First/Recurrent order rule is already in force. Some banks even never developed it and accepted both. But best is to wait till that day to adapt your systems.

As a summary the 20th of November will bring the following benefits:

- No difference anymore between a First and Recurrent

- No longer “incorrect sequence type” messages

- Creditors will be able to transfer SEPA Direct Debits closer to the execution time, especially for the First collection, which will reduce the risks of non-payment and will improve the quick detection of the possibility to effectively use a SEPA Direct Debit on the account of a customer.

- All transactions will be executed with the same timings, which will considerably simplify the use of SEPA Direct Debits.

More details can be found on the websites of several official organisations: